Retirement Security in a Pandemic, III: Invest for the long-term

Part Three of Three

Joslyn G Ewart, CFP® — September 15, 2020

There may be no better starting place for a discussion of Retirement Security in a Pandemic, III: Invest for the long-term, than a refresher regarding the marshmallow test. The marshmallow test was a study on delayed gratification led by Stanford University professor, Walter Mischel. The study offered young children two choices: one immediate small reward—a marshmallow—or, two small rewards if they waited for a period of time before eating their treat(s). Investing for the long-term is about aiming for the two (or more!) rewards by waiting first.

There may be no better starting place for a discussion of Retirement Security in a Pandemic, III: Invest for the long-term, than a refresher regarding the marshmallow test. The marshmallow test was a study on delayed gratification led by Stanford University professor, Walter Mischel. The study offered young children two choices: one immediate small reward—a marshmallow—or, two small rewards if they waited for a period of time before eating their treat(s). Investing for the long-term is about aiming for the two (or more!) rewards by waiting first.

No matter your age, generation, whether you are building wealth for the day you make work optional, or are currently retired, time is your friend when it comes to your investments. So, too, are risk and compound returns. In fact, time, risk, and compound returns are such important concepts forming the foundation of investment success that I name them investing BFF’s (best friends forever) in my book, Balancing Act: Wealth Management Straight Talk for Women.

Invest for the long-term

Part I of this series, Retirement Security in a Pandemic, delineated how to Lead with savings. Part II discussed a method to Plan based upon your values and prioritized goals. Part III of this series: Invest for the long-term, will discuss where to focus your attention as you aim for investment success unhindered by the shifting sands of current events. It is important to emphasize here that it is easy to maintain confidence in your portfolio strategy when capital markets are rising. On the other hand, it may require an increasing degree of intention on your part to maintain that same healthy confidence, when markets are dropping or are extremely volatile.

Your success is based upon faithful focus on what can provide investment success: time, risk, and compound returns. Please note that second-guessing yourself, reacting to capital market “noise,” and responding to persuasive media advice are not on the list of time-tested components for achieving the lifelong investment results to which most investors aspire.

Time can be essential to results because the longer you have your money invested, the more time it has to appreciate. This may sound simplistic but it is the reason we encourage investors to save early and often, rather than to let other priorities slip into first place and then “wait” until closer to retirement to start preparing. And while you may not add to your investments upon retiring, your portfolio can continue to appreciate while you are withdrawing the income you need to enjoy life.

Risk is a tough one for many investors. It can provoke the desire for a sense of control over fluctuating investments that just does not exist. The capital markets are dynamic; investors who embrace this fact, and recognize that the upward fluctuations make it worth—over time—putting up with the occasional down periods, have the opportunity to truly build wealth. This is true even if they start from the beginning with a modest investment of just $1,000.

Compound returns allow us investors to earn profit not only on the dollars we invest over time but also on each gain in our portfolios as time unfolds. This phenomenal feature of the dynamic nature of the capital markets is a perfect illustration of the concept: “win-win.”

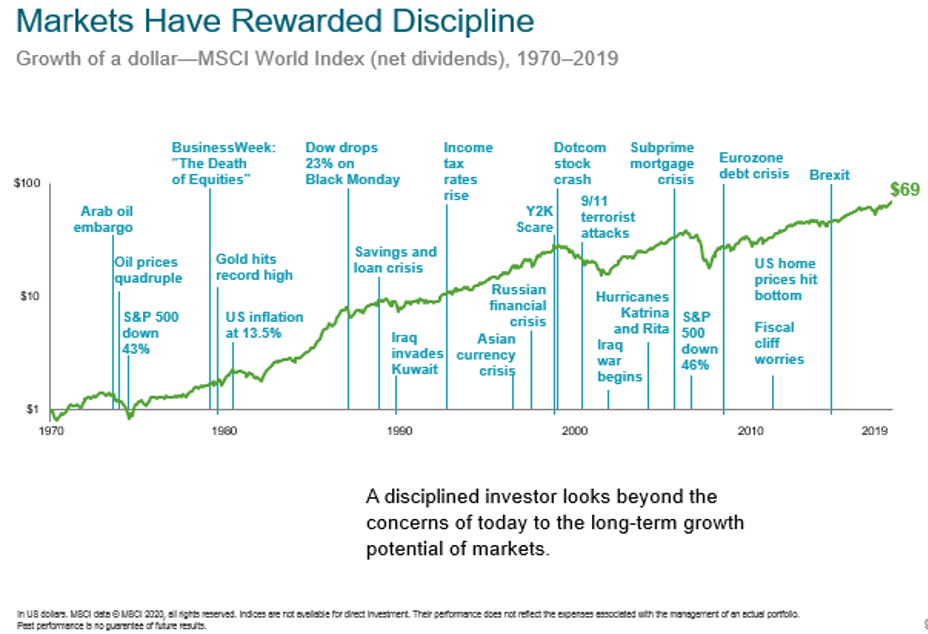

It is time for a picture that is worth a thousand words. I invested my first dollar in 1976. As the image below shows, the markets were then at rock bottom. Like most employees, my best savings opportunity was to contribute incrementally to my employer supplemental plan. In many cases, this type of plan is a 401(k) plan. Had I been able to make a single $100,000 investment in 1976, rather than incremental contributions over decades, note my portfolio would appreciate to $6,900,000 by the close of 2019. Yep. Time + risk + compound returns transform your money into WEALTH—wealth that is worth the intention, planning and patience required to achieve it.

The purpose of this series of three articles discussing Retirement Security in a Pandemic is to provide an overview of the three fundamental components that contribute to retirement financial security, the pandemic notwithstanding. Utilizing these three components: 1) Lead with savings; 2) Plan based upon your values and prioritized goals; 3) Invest for the long-term can make all the difference with respect to the success and security of your retirement plan.

Our intergenerational Entrust advisors—Baby boomer, Generation Xer, and Millennial—discover time and again that clients on track for retirement security, or those already retired with no money worries, also experience enhanced quality of life including the freedom to pursue the interests they value most. We welcome learning what is on your mind and responding to any questions you may have with respect to your retirement planning.

{kind=link}

{kind=link}

{kind=link}